S&P Global has revised India’s GDP growth forecast for the fiscal year 2025-26 downward by 20 basis points to 6.5%. The global credit rating agency cited rising protectionism, including rising US tariffs, and a broader pushback against globalisation as key external factors behind this downgrade. As India strives to retain its position as one of the world’s fastest-growing major economies, it must navigate a complex set of challenges to achieve its ambitious goals.

While the revised forecast still aligns with last year’s actual growth, it falls short of the earlier 6.7% projection, pointing to emerging hurdles. In its Asia-Pacific Economic Outlook, S&P noted that India’s resilient, services-led exports to the US remain a bright spot, but a combination of internal and external pressures could derail the country’s growth trajectory.

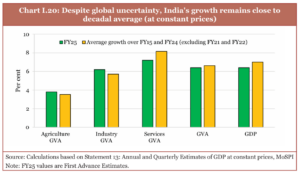

READ | SEBI kicks off high-stakes drive to reclaim trust

Trade tensions and global slowdown

The strongest external headwind comes from a sluggish global economy, struggling amid rising trade tensions. Slower international growth, fuelled by tariff hikes and geopolitical friction, is already weighing on global exports. Much of this has been attributed to US President Donald Trump’s aggressive trade policies, including higher tariffs on China, Canada, the EU, and India. Tariffs on Chinese imports, for instance, have climbed from an average effective rate of 25% to 35%, disrupting global supply chains and weakening demand.

Though India’s services exports to the US are expected to remain relatively unaffected, the broader indirect impacts are inevitable. Export-driven economies like China, Malaysia, Singapore, and South Korea are already feeling the pinch, and the spillover effects could dim India’s broader trade outlook. Exports remain a vital engine of India’s growth, contributing significantly to GDP and employment. The prospect of falling exports is therefore a serious concern.

Uncertain monsoon and vulnerable agriculture

The S&P report also highlights climatic risks, especially the critical role of the monsoon in sustaining India’s agricultural sector. Although the current forecast assumes a normal monsoon season, this remains a precarious assumption.

The Reserve Bank of India, in its latest bulletin, underlined how the growing frequency of extreme weather events is rendering Indian agriculture increasingly vulnerable. Given India’s heavy reliance on the monsoon, a poor season could severely dent agricultural output, push up food inflation, and erode rural purchasing power—a key driver of domestic consumption. A recent study by the European Central Bank also warned that global warming will likely stoke inflation, especially in emerging economies like India.

Geopolitics, oil prices, and import costs

S&P’s outlook factors in relatively soft commodity prices, especially crude oil, to support India’s growth estimate. But India, as a net importer of oil, is highly exposed to global price fluctuations. Escalating geopolitical tensions in West Asia and supply disruptions could easily spike oil prices, inflating India’s import bill and widening its current account deficit. This would have a knock-on effect on inflation and potentially nullify the gains from lower borrowing costs and tax incentives provided in the FY26 budget. Unfortunately for policymakers, managing this external variable lies largely outside India’s control.

While the Union Budget 2025-26 introduced tax incentives to encourage discretionary consumption, it also raises concerns about fiscal sustainability. India’s fiscal deficit remains elevated, and an over-reliance on stimulus measures could push up borrowing costs, crowd out private investment, and weaken long-term macroeconomic stability. Maintaining a delicate balance between short-term growth stimulus and long-term fiscal prudence is critical. Any lapse in discipline could dent investor confidence and slow down private-sector contributions to economic growth.

Inflation and interest rate dilemma

S&P projects that the RBI may cut interest rates by 75 to 100 basis points, capitalising on easing food inflation and stable oil prices to bring headline inflation closer to the 4% target. However, this optimistic scenario is heavily assumption-driven. Food inflation, in particular, remains a stubborn concern and could spike again due to monsoon variability or supply disruptions.

In such a case, the central bank may be forced to prioritise price stability over growth, as seen in the past. This would limit its ability to cut rates further, thereby restricting efforts to boost consumption and investment, both of which are crucial to achieving the 6.5% growth target.

Some of the risks mentioned also serve as supportive factors. For example, easing inflation, budgetary tax incentives, and an expected decline in borrowing costs are all likely to boost consumer spending in the short term. But this fragile optimism must be viewed through the lens of global volatility and domestic constraints.

GDP growth: Structural challenges persist

Beyond immediate problems, India faces structural barriers such as inadequate infrastructure and persistent unemployment. A slowdown in government capital expenditure (capex) was one of the main reasons behind the second-quarter growth dip. A revival in public capex is essential. According to Deloitte’s India Economic Outlook (January 2025), the government must allocate more funds to infrastructure and ensure better capex utilisation by the states.

Rising unemployment and underemployment also threaten to curb consumption and fuel social unrest, further endangering economic stability. This is particularly troubling as India aims to position itself as a manufacturing and digital powerhouse. However, some economists believe that India’s demographic dividend and expanding middle class offer long-term potential for stronger consumption and labour market resilience.

To unlock higher productivity and attract sustained investment, India must pursue structural reforms in labour laws, land acquisition, and agriculture. Equally crucial is the need to harness the demographic dividend by creating more jobs and improving skill development. Without these measures, the demographic advantage could turn into a burden.

India’s medium-term growth outlook remains promising, but the road ahead is riddled with external shocks, policy dilemmas, and structural vulnerabilities. Policymakers must act decisively to address both short-term risks and long-term constraints. The challenge lies in navigating this complex landscape while ensuring inclusive and sustainable growth.