India’s banking industry, which recently experienced a period of remarkable performance, now stands at the crossroads of opportunity and challenges. As the New Year unfolds, banks face a complex situation marked by pressures on margins, regulatory changes, and evolving credit dynamics.

The Reserve Bank of India is expected to announce a series of repo rate cuts in 2025 which could provide temporary relief to banks by reducing their funding costs. However, the immediate repricing of external benchmark-linked loans due to these cuts, juxtaposed with the gradual adjustment of deposit rates, is likely to exert significant pressure on net interest margins. Private banks, with their larger share of external benchmark-linked loans, are particularly vulnerable to these dynamics.

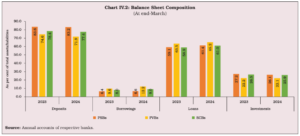

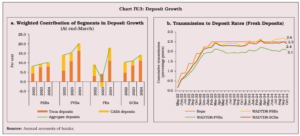

Despite these challenges, the overall financial health of the sector offers a silver lining. Banks’ strong balance sheets serve as a buffer against margin pressures. Yet, the slow decline in deposit rates, even as lending rates decrease, is likely to make resource mobilisation a persistent challenge. This issue is compounded by the elevated cost of raising deposits. Banks will need to adopt innovative strategies to ensure efficient resource mobilisation without further impacting profitability.

READ I Private capital expenditure: The missing link in India growth story

Banking Industry awaits regulatory overhaul

The banking industry is poised to undergo significant regulatory transformations in 2025. These include the phased implementation of Expected Credit Loss (ECL) norms, revised liquidity coverage ratio (LCR) requirements, and new project financing guidelines. While these changes aim to enhance financial stability and resilience, they bring immediate challenges for banks.

Under the ECL framework, banks are required to recognise stress earlier, necessitating higher provisions. This shift is expected to impact profitability in the short term, with provisions potentially increasing from 2% by March 2025 to 5% by 2027. Additionally, the LCR requirements, which include a 5% increase in runoff factors for retail deposits enabled by digital banking, are likely to tighten liquidity further. This could slow credit growth and exert additional pressure on NIMs.

Project financing, particularly for under-construction infrastructure and real estate projects, will also face stricter provisioning requirements, which could lead banks to adopt a more cautious approach. Public-sector banks, often more exposed to infrastructure financing, may find these norms particularly challenging. However, experts say that the sector’s robust health positions it to absorb these regulatory shocks.

Asset quality under pressure

India’s banking industry has achieved remarkable progress in improving asset quality over the past few years. The gross non-performing asset (GNPA) ratio has dropped below 3%, a significant improvement from its peak of over 20% in 2018. Public-sector banks, in particular, have seen their GNPA ratios fall from 14.2% in 2018 to 3.15% in 2024, narrowing the gap with private banks.

However, challenges persist in the retail and unsecured loan segments. Rising stress in unsecured loans, such as personal loans and credit cards, is expected to marginally increase retail NPAs. The microfinance segment is also grappling with tight liquidity and over-leveraging, signalling prolonged challenges. As banks recalibrate their strategies, the narrowing asset quality gap between public and private banks stands out as a positive development, reflecting the sector’s resilience.

Slowing credit growth

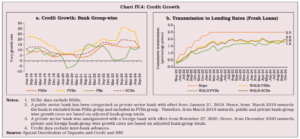

Credit growth, a critical driver of banking profitability, has significantly slowed, reaching a three-year low in 2024. This trend is driven by several factors. Tight liquidity conditions, coupled with slower deposit growth, have constrained banks’ ability to lend. Additionally, high inflation and elevated interest rates have deterred corporate borrowing, exacerbating the slowdown.

Leadership transitions at key banks, including IndusInd Bank, Indian Bank, and Punjab & Sind Bank, add another layer of complexity. While new leadership could bring fresh perspectives, the transition period may lead to temporary disruptions. To sustain growth, banks must explore innovative credit avenues and address structural liquidity issues. The narrowing credit-deposit ratio and reduced private capital expenditure further underscore the need for strategic realignment.

Retail lending remains stable

Amid the challenges facing the sector, the retail lending segment has demonstrated remarkable resilience. Stable flows from systematic investment plans (SIPs) and sustained interest from retail investors in the small-cap space have provided a degree of stability. However, the segment is not immune to pressure. Rising inflation and interest rates are likely to challenge the lending institutions operating in this space.

Unsecured retail loans, a significant growth driver for some banks, are showing signs of stress. Lenders such as IDFC First Bank, RBL Bank, and several small finance banks are already grappling with asset quality issues in this segment. These challenges underscore the need for cautious expansion and enhanced risk management practices in the retail lending space.

Increasing uncertainty

The year ahead will test the adaptability and resilience of India’s banking industry. Mobilising stable, low-cost deposits remains critical for mitigating margin pressures. Additionally, banks will need to adopt a more selective approach to project financing, focusing on risk mitigation and prudent lending practices.

Technological innovation will play a pivotal role in addressing operational inefficiencies and improving customer engagement. Digital banking solutions, combined with robust regulatory compliance, can help banks navigate the evolving landscape. Despite the challenges, large private banks like ICICI Bank and HDFC Bank are well-positioned for relative outperformance, while public-sector banks must address structural inefficiencies to remain competitive.

While the long-term prospects of the sector remain robust, stakeholders must prioritise sustainable growth, prudent risk management, and technological innovation to navigate the road ahead effectively. By addressing these challenges head-on, India’s banking industry can secure its place as a cornerstone of the nation’s economic growth.