Green hydrogen is emerging as an alternative energy source, gaining traction because of its environmental benefits. This advantage places hydrogen as a major factor in the global market for decarbonising sectors such as transportation, industry, and power generation. It also offers the aviation industry a sustainable fuel alternative.

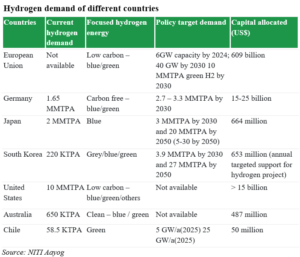

According to the International Renewable Energy Agency (IRENA), six players — the United States, South Korea, Japan, India, China, and the European Union — have the potential to become the world’s primary suppliers of green hydrogen. India, with the world’s third-largest economy in terms of energy consumption, expects a 35% increase in energy demand by 2030. The hydrogen demand of other countries is shown in Table 1.

Global collaboration is vital in advancing the hydrogen economy, with international partnerships and agreements playing a crucial role in standardising hydrogen production, storage, and transport technologies. Countries leading in hydrogen development are forming alliances to share knowledge, technology, and best practices, fostering a cohesive global approach to hydrogen adoption. Such international cooperation is essential for creating a unified market and regulatory framework that can facilitate large-scale hydrogen deployment and ensure its integration into the global energy mix.

READ I Rice subsidies: Rethinking food security in a globalised market

Big investments in green hydrogen tech

Japan, Australia, Chile, and Saudi Arabia are making significant technological investments, with the EU planning to invest $430 billion in green hydrogen by 2030. Portugal aims to start producing green hydrogen by the end of 2025, with €10 billion reserved for eight projects. India’s National Green Hydrogen Mission aims to make the country a significant hub for producing, exporting, and utilising natural resources, targeting 500 GW of renewable energy capacity and a one billion tonne cumulative reduction in emissions by 2030. The nation’s green hydrogen production capacity is expected to reach 5 million metric tons per annum, reducing fossil fuel dependency and creating over 600,000 jobs.

India’s strategic geographic location and abundant renewable resources give it a unique advantage in the green hydrogen market. With its vast coastline and solar irradiance, India can produce green hydrogen economically and potentially become a hub for hydrogen export to neighbouring countries and regions. Establishing regional hydrogen corridors can enhance energy security and foster economic growth, positioning India as a leader in the emerging green hydrogen economy.

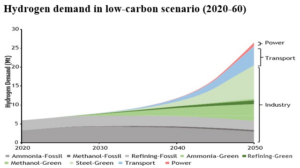

Green hydrogen is gaining momentum, especially in the steel, road transport, shipping, and aviation sectors. Achieving a net-zero target by 2060 may require around 40 Mt of green hydrogen, representing a sevenfold increase from today.

Green hydrogen is crucial for India’s climate strategy, offering a cost-effective decarbonisation solution for over a fifth of total energy consumption. This can lead to an 80Gt cumulative CO2 reduction, aligning with the 1.5°C climate scenario. Producing green hydrogen via electrolysis, which splits water into hydrogen and oxygen, requires a low-carbon energy source. Renewable energy accounts for nearly 70% of the investment needed for green hydrogen electrolysis. Currently, coal and oil supply 75% of India’s energy needs, a figure expected to rise. Therefore, integrating renewable energy with green hydrogen is essential for reducing fossil fuel reliance and optimising India’s solar potential, especially as solar energy costs have dropped to $2 per kWh.

However, green hydrogen faces challenges in transportation and storage due to its low volumetric density and high flammability, necessitating specialised infrastructure and leading to significant energy losses in the supply chain. Approximately 30–35% of the energy is lost during electrolysis, with additional losses during hydrogen liquefaction, conversion, and transport. Integrating hydrogen into the existing natural gas grid might require extensive new pipeline infrastructure.

To overcome these hurdles, a concerted cross-sectoral effort is needed, with governments playing a crucial role in developing policy frameworks to stimulate market demand, foster private investment, set conducive standards and regulations, and support research and development (R&D). India, leveraging its large population and growing energy needs, could become a key player in the hydrogen market, expanding its R&D investment, establishing relevant legislation, and building the necessary infrastructure to meet domestic demand and export hydrogen internationally.