With Budget 2024 round the corner, insurance firms are seeking multiple tax exemptions from the government to increase the appeal and affordability of insurance offerings. This is also expected to speed up the nationwide penetration of insurance products. The insurers are seeking tax cuts on annuities and a reduction in the GST rates applied to their products. The industry is optimistic that there will be a revision of the tax framework to reintroduce tax exemptions for life insurance products. Currently, under the new tax regime, these exemptions, previously available under Section 80C of the old tax regime, are not permitted.

India’s insurance sector on track for a strong growth

India’s insurance industry is experiencing steady growth, but challenges remain. It is the 10th largest globally, but life insurance penetration is still low at 3.2% (as of 2021 data). The insurance industry faces regulatory challenges that need to be addressed to facilitate smoother operations and growth. Streamlining regulatory processes and reducing bureaucratic hurdles can help insurance companies focus more on expanding their reach and improving their services. The Insurance Regulatory and Development Authority of India should continue to refine policies to support innovation and competition within the industry.

READ | Women-led rural enterprises key to fighting poverty, must get priority sector status

Why tax cuts on insurance premiums

In times of distress, insurance acts as a safety net. During medical emergencies, disability, or death, insurance provides a financial cushion and helps individuals better navigate the challenges at hand. Many Indians do not have enough savings for their post-retirement life, and there remains a huge gap between the funds available and the funds needed for a peaceful retirement.

Regarding health insurance, tax benefits exist for both health and life insurance premiums, but they are capped and often complex to navigate. Naturally, many with limited resources are dissuaded from prioritising insurance. Millions of citizens remain vulnerable to illness, disability, or unforeseen events in the absence of insurance. Current tax structures are often to blame.

While the government offers help in various forms, it is practically impossible for it to assist each individual. Unlike many other countries, India’s social safety net has a different structure. While some nations boast comprehensive social security programs, India’s options are more limited. Government initiatives like the PM Jeevan Jyoti Bima Yojana and PM Suraksha Bima Yojana offer some financial protection, but their scope is limited. Additionally, the PM Jan Arogya Yojana provides health insurance coverage of up to Rs 5 lakh per family, but eligibility is restricted to those below a certain income level.

To address this, significantly increasing the tax deductions allowed for premiums paid towards health and life insurance may be a way forward. Simplifying the tax benefit structure for insurance will make it easier for all, regardless of their tax bracket or financial literacy, to understand and avail of these benefits.

Additionally, the insurance sector must leverage technology to enhance accessibility and affordability. Digital platforms can play a crucial role in simplifying the purchase process, providing real-time assistance, and enabling quick claim settlements. By investing in digital infrastructure, insurance firms can reach a broader audience and provide seamless services, thus encouraging more people to opt for insurance coverage.

High out-of-pocket medical expenses in India presently exceed global averages. More than 50% of healthcare expenses are paid directly by patients. This reveals an abysmal lack of financial protection for citizens. The insurance regulator must set an ambitious goal of Insurance for All by 2047. Insurance companies also await reforms in several key areas such as better implementation, increased participation from multi-specialty and corporate hospitals, and improved outreach to the underprivileged Below Poverty Line (BPL) population.

By encouraging insurance participation through tax cuts, the government does not simply lessen its social security burden; it empowers citizens to take charge of their own well-being. This creates a more responsible and financially secure society, ultimately benefiting the nation as a whole. Presently, health insurance attracts GST rates of 18%. A reduction of the same to 5% will make these products more affordable, leading to greater uptake. When GST is charged on insurance services, it is automatically added to the insurance premium as an additional tax. This is why policy premiums have been increasing.

Tax breaks are crucial for individual taxpayers. Currently, health insurance premiums feel like an optional expense compared to a necessity, especially considering the cost of family plans versus the limited tax benefit. Individual taxpayers need a tax impetus because family health insurance premiums versus the tax benefits are skewed.

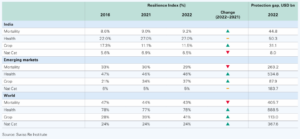

India insurance resilience indices and protection gaps

Furthermore, the role of insurance in promoting financial inclusion cannot be overstated. By making insurance products more affordable and accessible, the government can help integrate marginalised sections of society into the financial mainstream. This not only provides financial security to vulnerable populations but also stimulates economic growth by fostering a more resilient and inclusive financial ecosystem.

A critical area that requires attention is the disparity in insurance penetration between urban and rural areas. Urban regions tend to have higher awareness and uptake of insurance products due to better access to information and services. However, rural areas, which constitute a significant portion of the population, lag behind. The government and insurance firms must work together to bridge this gap by offering targeted awareness campaigns and simplified insurance products tailored to the rural population’s needs.

The government should issue more long-term bonds (40-50 years) to increase liquidity. This benefits insurers by offering more investment options and potentially lower interest rates for their long-term liabilities. Additionally, the corporate bond market should allow insurers to invest in reliable, long-term corporate bonds. These bonds could offer higher yields than traditional government bonds, potentially enabling insurers to provide better returns on annuity plans.